The Asia-Pacific Refrigerant Market is witnessing robust expansion, driven by increasing demand for air conditioning, refrigeration, and heat pump systems across residential, commercial, and industrial sectors. As rapid urbanization, industrialization, and climate change heighten the need for efficient cooling systems, the region is becoming the global epicenter of refrigerant consumption and innovation.

In 2024, the Asia-Pacific refrigerant market was valued at USD XX billion, and it is projected to reach USD XX billion by 2033, growing at a CAGR of XX% during the forecast period (2025–2033). The growth is primarily attributed to expanding HVAC (Heating, Ventilation, and Air Conditioning) installations, the booming automotive industry, and the ongoing transition toward low-GWP (Global Warming Potential) and eco-friendly refrigerants.

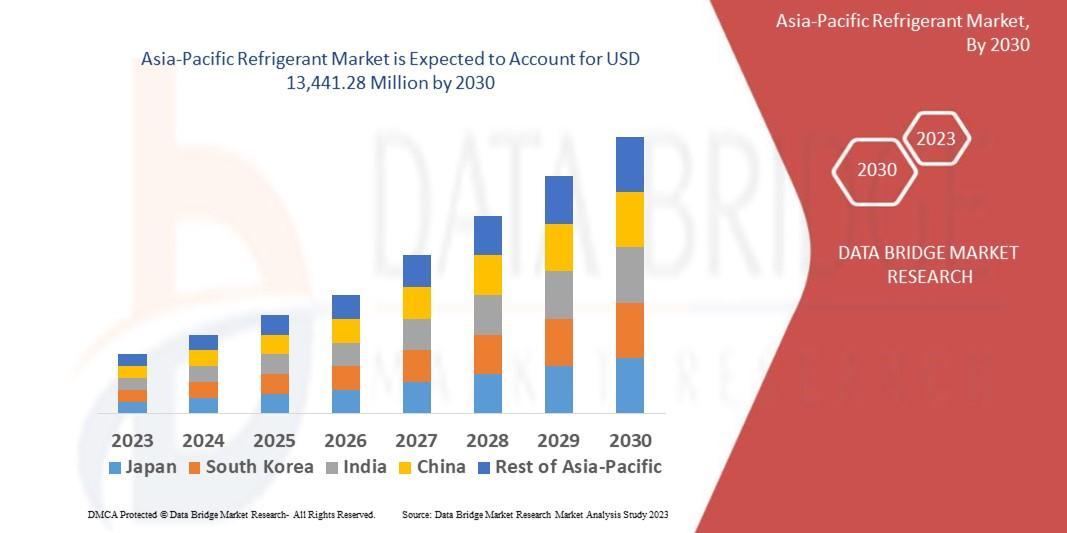

Find out what’s next for the Asia-Pacific Refrigerant Market with exclusive insights and opportunities. Download full report:

https://www.databridgemarketresearch.com/reports/asia-pacific-refrigerant-market

Market Dynamics

1. Market Drivers

a. Rapid Urbanization and Rising Disposable Incomes

The Asia-Pacific region, led by China, India, Japan, and South Korea, has seen a dramatic rise in living standards and urban density. The expanding middle class demands higher comfort levels, resulting in surging adoption of air conditioning systems, refrigerators, and cold storage facilities.

b. Growth in Cold Chain Logistics

The region’s growing demand for perishable food products, vaccines, and pharmaceuticals is fueling investment in cold chain infrastructure. This sector heavily relies on refrigerants for temperature control, accelerating market growth.

c. Expansion of the Automotive Sector

With automotive manufacturing hubs in China, India, Japan, and Thailand, the demand for mobile air conditioning systems (MAC) is increasing. This has driven consumption of refrigerants such as R-134a, R-1234yf, and R-744 (CO₂).

d. Climate Change and Extreme Weather

Rising global temperatures are escalating cooling needs across tropical and subtropical regions of Asia-Pacific. This has intensified the demand for energy-efficient and environmentally sustainable refrigerants.

2. Market Restraints

a. Regulatory Challenges

Stringent environmental regulations like the Kigali Amendment and regional phase-down plans for HCFCs and HFCs are forcing manufacturers to transition toward alternative refrigerants. While necessary for sustainability, this shift increases production costs.

b. Flammability and Toxicity Concerns

Natural refrigerants such as ammonia (NH₃), propane (R-290), and isobutane (R-600a) pose flammability or toxicity risks, creating challenges for large-scale adoption without advanced safety systems.

3. Market Opportunities

a. Shift Toward Low-GWP Refrigerants

With countries pledging to reduce carbon emissions, the demand for low-GWP hydrofluoroolefins (HFOs) and natural refrigerants is rising. Investments in sustainable cooling technologies are opening new revenue streams.

b. Technological Advancements

The development of next-generation refrigerants with improved thermodynamic efficiency and lower environmental impact offers strong opportunities for innovation and market leadership.

c. Government Incentives and Green Policies

Regional governments are promoting eco-friendly refrigerant adoption through subsidies, tax benefits, and green building certifications—creating a favorable ecosystem for market expansion.

Market Segmentation

By Type

-

Hydrochlorofluorocarbons (HCFCs)

-

Gradual phase-out due to high ozone depletion potential.

-

-

Hydrofluorocarbons (HFCs)

-

Still dominant but under regulation for high GWP.

-

-

Hydrofluoroolefins (HFOs)

-

Gaining popularity as next-gen sustainable refrigerants.

-

-

Natural Refrigerants

-

Includes ammonia, CO₂, hydrocarbons, and water-based alternatives.

-

By Application

-

Refrigeration

-

Commercial refrigeration, supermarkets, cold storage, and food processing.

-

-

Air Conditioning

-

Residential, commercial, and automotive sectors dominate consumption.

-

-

Heat Pumps

-

Increasingly adopted in sustainable building solutions.

-

-

Chillers and Industrial Processes

-

Used in manufacturing, petrochemicals, and industrial cooling systems.

-

By End User

-

Residential

-

Commercial

-

Industrial

-

Transportation and Automotive

Regional Insights

China

China holds the largest share of the Asia-Pacific refrigerant market. The country is a global leader in refrigerant manufacturing, with robust domestic demand for HVAC and refrigeration systems. Its transition toward R-32, R-290, and CO₂-based systems underlines its commitment to sustainable cooling.

India

India’s refrigerant market is expanding rapidly, driven by infrastructure development, retail expansion, and cold chain modernization. Government initiatives like “Make in India” and rising adoption of energy-efficient air conditioners are fueling growth.

Japan

Japan is at the forefront of eco-friendly refrigerant technology, focusing on low-GWP and zero-ODP alternatives. The nation’s mature HVAC industry continues to innovate with HFOs and CO₂ systems.

South Korea and Southeast Asia

Emerging economies such as Thailand, Indonesia, Vietnam, and Malaysia are experiencing fast-paced growth in commercial refrigeration and automotive air conditioning. These markets are transitioning gradually toward HFOs and natural refrigerants.

Competitive Landscape

The Asia-Pacific refrigerant market is moderately consolidated, with both global chemical giants and regional manufacturers competing for market share. Key players focus on expanding product portfolios, strategic partnerships, and sustainable innovations.

Key Companies

-

Daikin Industries Ltd.

-

Honeywell International Inc.

-

The Chemours Company

-

Arkema S.A.

-

Linde plc

-

Dongyue Group

-

Sinochem Group

-

SRF Limited

-

Navin Fluorine International Ltd.

-

AGC Inc. (Asahi Glass Company)

Strategic Developments

-

Leading firms are investing in next-generation HFO refrigerants.

-

Mergers and partnerships aim to strengthen distribution networks and manufacturing capabilities.

-

Companies are collaborating with HVAC manufacturers for green cooling technologies and regulatory compliance.

Regulatory Landscape

The refrigerant industry in Asia-Pacific is evolving under global and regional environmental mandates such as:

-

Kigali Amendment to the Montreal Protocol – Targets HFC phase-down.

-

India’s Ozone Depleting Substances (Regulation and Control) Rules.

-

China’s HFC control measures under the “Dual Carbon” goal.

-

Japan’s Act on Rational Use and Proper Management of Fluorocarbons.

These frameworks promote sustainable practices while encouraging innovation in refrigerant chemistry and recovery technologies.

Future Outlook

The Asia-Pacific refrigerant market is transitioning toward sustainability and innovation. With the push for carbon neutrality, smart cooling systems, and green building standards, the region will lead the global refrigerant transformation over the next decade.

Key trends shaping the future include:

-

Expansion of natural and low-GWP refrigerants.

-

Growth of AI-integrated HVAC systems for energy optimization.

-

Increasing investment in circular economy models, including refrigerant recovery and recycling.

Key Takeaways

-

Asia-Pacific dominates the global refrigerant market, with rapid growth expected through 2033.

-

China and India remain the largest growth engines, supported by industrialization and climate-driven cooling needs.

-

Sustainability and regulation compliance are reshaping the market toward low-GWP and natural refrigerants.

-

Technological advancements in refrigerant efficiency and system integration will define competitive advantage.

Conclusion

The Asia-Pacific Refrigerant Market stands at the forefront of the global cooling revolution. Balancing rapid industrial growth with environmental responsibility, the region is shifting from traditional HFCs toward next-generation, climate-friendly refrigerants. As nations strengthen regulatory frameworks and consumers demand greener technologies, manufacturers that innovate early in sustainable refrigerant solutions will gain a decisive competitive edge in the decade ahead.

Browse More Reports:

Global Water Treatment Chemicals Market

Global Ceramics Market

Global Gemstones Market

Global Smart Fleet Management Market

Global Tote Bags Market

Global Tuna Market

Global Cataracts Market

Global Kimchi Market

Global Party Supplies Market

Global Plant-Based Food Market

Global Processed Fruits Market

Global Wearable Devices Market

Global Commodity Plastics Market

Global Dehydrated Food Market

Global Hepatocellular Carcinoma Drugs Market

Asia-Pacific Natural Terpenes Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com